2021 Predictions #7 The Next Big Shooter is...

This analysis is written by Michail Katkoff, Adam Telfer, Ionut Dogaru, and Alexandre Macmillan.

Access all of our previous predictions. Signup for the newsletter. Apply for our Slack group.

Our 2021 predictions have been sponsored by Facebook Gaming.

Facebook Gaming helps developers and publishers to build, grow, and monetize their games. This is done through in-depth research, insights, and case studies as well as innovative marketing solutions and education materials.

Visit Facebook Gaming where you’ll find an incredible amount of insightful, actionable, and relevant information along with tips, tools, and solutions to help you grow your business.

Unless otherwise specified, all the data has been provided by the powerful Sensor Tower and analyzed by the author(s). All revenue numbers show net revenues. Data from China, Korea, and Japan are excluded as this analysis focuses on Western markets only.

Finally, please take the numbers presented with a giant grain of salt. They are meant more for trend analysis based on estimations, rather than exact figures.

Shooters are the fifth largest genre on mobile at $2.1B in net revenues during 2020, while holding the top games on mobile. What makes the genre so interesting is its growth of both revenue and installs. During 2020 the revenues boomed by 38% Year-over-Year while the installs clocked at 2.7B, growing by 31% compared to 2019.

Revenues from China, Japan and Korea are excluded. With those in, the shooter genre would be significantly larger.

What caused all engagement to jump through 2020 gave the entire shooting category arguably some of the strongest tailwinds. In a category that demands full player focus, high session length, and a stable internet connection, only the Casino category benefited more from stay-at-home orders.

Adding to the increased download share, increased engagement is mixed with its fair-play cosmetic only economy. You see, the largest games in the category are all cosmetic focused, and when engagement increases in cosmetic focused economies, revenue jumps in lockstep.

All this is fueled by some of the heaviest live content operations in the industry. On top of the content treadmill demanding hundreds of cosmetics needed to fuel the monetization, these top mobile shooter games demand brand new gameplay modes and events at a fast cadence. To keep players coming back each season, each event -- there needs to be gameplay impacting content for players to enjoy. This year was a testament to how important that content was. PUBG Mobile, COD Mobile, Garena Free Fire, Fortnite, and Knives Out each came out with phenomenal game modes and cosmetics that kept players coming back. These games were rewarded with some of the best retention curves in the industry.

Shooter games are known for some of the heaviest live content operations in the industry.

Image: Garena Free Fire

And all this is ignoring the game we were all obsessing over in 2019: Fortnite. The 38% revenue growth as a category happened despite the massive hole created when Fortnite left the AppStore on August 28th. For a third of the year, one of the biggest games in this category vanished. So just imagine what growth rate we COULD have seen if Tim Sweeney hadn’t started his crusade?

All this wraps up into a massive and growing genre that is dominated by the top developers in our industry. A category that is riding the market shift that players want deeper, more social, more connected experiences.

How to Find Blue Spots in the Red Ocean?

Some of the biggest games and game franchises in the world are shooters. And what makes this category of games even more remarkable is that some of these most prominent shooter games have been released not too long ago. While Call of Duty has been a household name for two decades, Fortnite, PUBG and Garena Free are relative newcomers that have transformed their publishers into global powerhouses.

The shooter gold rush in the Western markets was ignited by the launch of battle royale games in 2018. The big question is whether the gold rush is over? Has the market matured to a point where the entry is allowed only to gigantic game teams (preferably in low-cost locations) that churn out immense amounts of content to their battle passes and add constantly new gameplay modes for their tens of millions of daily active players?

When it comes to competitive shooters that monetize through the cosmetics driven economy, the gold rush, in our opinion, ended in 2019. But when it comes to the shooter category in general, we believe that there are ways to succeed in the market because and due to the three reasons below.

#1 Strong demand

A shooter game on average reaches 20M installs on mobile during its life-time. That’s a very high number of downloads given that the average shooter is made by a relatively small studio that lacks an IP or the publishing muscles to justify the downloads.

Shooters on mobile are download magnets. Not just the big ones.

#2 Underpricing has created an entry barrier

Mobile shooters are categorized by high levels of installs and below-average CPIs. At the same time, the focus on competitive PvP in a shooter sets a limit on monetization. Most shooter titles exclude power progression, which is the cornerstone of free-to-play monetization, and instead focus on selling cosmetics via content-heavy battle passes.

Underpricing is the winning strategy for the big players in the shooter category. Tencent and Garena simply underprice by offering ludicrous amounts of content that only they can produce with 200-300 head studios. There's no pinch, ever. And that's what produces the strong retention curves, which leads to healthy long-term monetization.

The big Asian studios create entry barriers by offering a superior service at a price that is lower than the players would likely be willing to pay. As a result, newcomers are unable to compete as they don’t have an audience and they can’t charge a premium to invest in building that audience.

The effectiveness of the underpricing strategy is evident when we look at the revenue trends. The overall revenue is up by a whopping 38%. While the top 4 shooter games had a much smaller slice of the growing downloads pie they grabbed 90% of all revenue in the category up from 75% a year ago.

While the top 4 shooter games had a much smaller slice of the growing downloads pie they grabbed 90% of all revenue in the category up from 75% a year ago.

#3 Underserved audience

Content-rich battle passes, steady addition of new maps and game modes as well as the incentive to play with friends feed into the retention of a modern shooter game. Yet not all players enjoy the extremely competitive player versus player where losing is more common than winning.

Apart from the Sniper games, all shooter genres on mobile pit players in direct competition. And while they incentivize players to collaborate, only a few of them offer character classes and ways for players to specialize. Most importantly though, the lack of any form of power progression puts all the emphasis on skill and thus can become off-putting for more mature audiences that can’t keep up with the young guns.

We’ve seen PUBG come up with the Metro Royale game mode and NetEase launch Badlanders. Both of these put an emphasis on the gameplay around session-to-session and offer a certain level of power progression. Nevertheless, the ultra-competitive nature bundled

Find the Blue Spot

There’s strong demand for new shooters, as we can see from the downloads. Yet it is nearly impossible to compete with the existing powerhouse in the category that wins by offering superior service at a lower perceived price.

On the console and PC side, we’ve seen the shooter genre evolve much further than it has on mobile with games like Borderlands 3, Vigor, Warframe, and Escape from Tarkov all finding their own position in the category through both gameplay and meta-game innovations. Think like Tarkov and Warframe: to compete in this genre means picking your “blue spot” in this red ocean.

Shooters on Mobile in 2020

We’ve broken Shooters into 4 sub-categories:

Multiplayer Shooters (FPS/3PS) categorized by PvP action (example: Call of Duty)

Battle Royale (example: PUBG, Fortnite) which technically could be considered a subcategory within Multiplayer Shooters, yet it was worth carving out due to its popularity,

Tactical Shooters where the speed of action is far more slower and typically involves pay-to-progress mechanics (example: World of Tanks)

Sniper games where the player is only shooting and not moving (example: Sniper 3D). Let’s go through each in order.

Sniper games, which kicked off the shooter genre, have become a mature niche. Its growth is significantly lower than the shooter genre as a whole.

Tactical team-based shooters, like War Robots and World of Tanks, was the genre that emerged after Snipers. The genre experiences healthy growth with a 31% increase in 2020.

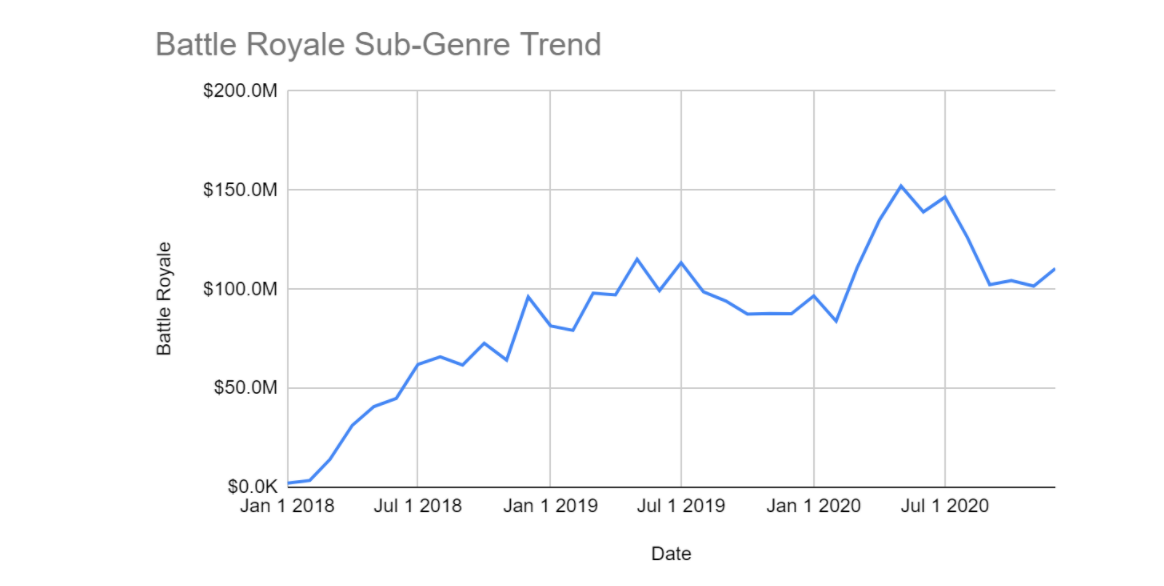

Then there are the Battle Royale games that burst into the scene in 2018. The installs remained largely unchanged when comparing 2020 to 2019. At the same time, revenues continued to climb at a very considerable pace. But there are two things that need to be pointed out: 1) PUBG brings nearly 60% of all genre revenues and 60% of PUBG’s revenues ($1B) are coming from China. 2) Fortnite’s Android revenues are partial and iOS revenues were cut to zero in August 2020.

The revenue of First-Person and Third Person (FPS/TPS) Shooters nearly doubled over last year. Call of Duty Mobile was the title driving most of the growth. The game quadrupled its revenues over the year while also being responsible for three out of four dollars made by the games in this sub-genre. We expect FPS/TPS Shooters to continue to grow, but more about that in the analysis below.

Battle Royale

Battle Royale has been in the “it” category for over 2 years now. However, it’s no longer the “new” thing. That hasn’t stopped developers from adding Battle Royale to nearly every genre it can (Tetris Royale? Mario Royale?) but the reality is that Battle Royale Shooters have captured something those other genres have not. A Battle Royale shooter has some of the strongest retention curves in gaming. That’s despite the complex controls, insane matchmaking of 100 players, and long match times.

Similar to the shooting category, 2020 was a year of growth for Battle Royale, across PC and console. Battle Royale games were the destination kids went to during stay at home orders (Roblox and GTA Online being the other beneficiaries). Battle Royale has matured, but 2020 stabilized and grew that engagement.

Looking at the Top 5 in this category for the west, we can see that PUBG continues to reign supreme. However, its Tencent-backed buddy, Garena’s Free Fire, is catching up fast. They had a phenomenal year, outpacing PUBG and Call of Duty’s RPI growth through 2020. More on them in our predictions.

The second notable change is Zooba by Wildlife Studios. We mentioned it in last year’s post:

“Going casual .. will avoid the big players like Tencent and Activision -- but thus far the game has failed to retain and monetize at the same level. “It’s likely this game is able to carve out its own niche away from Tencent - by focusing casual and focusing on Wildlife’s growth expertise in lower tier markets, but will operate at the low end of the CPI:LTV spectrum”

And this pretty much happened. It looks like they were able to carve out their own niche of mobile players, drive significant downloads. Likely the revenue number here doesn’t capture the ad revenue on top. But Zooba isn’t operating at the same tier as Fortnite, Garena, and PUBG -- despite it selling gameplay impacting upgrades. This just goes to show that if you can operate cosmetics and events at the same level as Tencent, you can reach far higher LTV numbers than a more “traditional” pay-for-power economy. However, you just need one of the largest cosmetics pipelines in this industry to accomplish that. Well done for Wildlife for carving out their niche and slowly growing through 2020.

But battle royale is likely over its peak of new player growth now, into its maturity phase. The Battle Royale trend has fizzled, and while it is left in its wake some of the best sustaining services (PUBG Mobile, Warzone, Fortnite, Free Fire), players have started to become tired of Battle Royale and are starting to seek out new types of experiences. TiMi, Lightspeed & Quantum, Epic, and Garena have been smart -- slowly adding new game modes and finding ways to introduce novelty.

The winners this year for introducing novelty have to be Fortnite and PUBG Mobile. Fortnite with its “Spy Within” Mode -- which quickly caught on to the trends of Among Us and Transmaphobia, and quickly introduced a similar mode to the game -- alongside cosmetic rewards for pushing players to try it out.

PUBG Mobile launched Metro Royale, a “looter shooter” version of their game, which fundamentally shifted how players played. Taking notes from Battlestate’s “Escape from Tarkov” and Bohemia’s “Vigor”, they added actual progression to a battle royale! Now instead of losing all your loot at the end of the match, the goal of a match becomes collecting as much loot as possible and exiting the map without getting killed. This feels like betting mechanics on steroids -- each match is a roll of the dice whether you’ll be able to get out with the loot you want.

The history of the genre points to where this genre is moving to. Going back to Day Z, Vigor, H1Z1 -- this is a survival genre first and foremost. Within the design space of a multiplayer server instance with hundreds of synchronous players, the potential to have AI encounters in the space, and the drive to collect through looting -- Battle Royale has been amazing but is by no means the end of design. Teams within Battle Royale will be experimenting each season with introducing new game modes that can feel just as exciting. It will be an interesting genre to watch!

First Person and Third Person Shooters

Separate from Battle Royale, we’ve carved out an FPS/TPS sub-genre. These games are focused on modes like team deathmatch and often default to the first-person view due to their competitive nature. Within this group, Crossfire (originally a 2007 PC game) has been dominant up to fall 2019, when Call of Duty Mobile was launched.

The shooter market in 2020 in the West was really all about CoD’s growth. The game had a fantastic launch in late 2019 becoming the highest downloaded game of all time. But its revenue generated per player was weak in comparison to other cosmetic-only economies. Given the strength of the studio behind the game (TiMi Studios), we predicted last year that 2020 will be the year when Tencent and Activision ramp up the monetization in CoD Mobile. And boy were we right…

Call of Duty Mobile’s revenues jumped up by 362% compared to 2019. Now partially this is due to the fact that CoD launched in late 2019 and thus accumulated only a fourth of the revenues for the year. The real reason behind the growth is the quality of updates that we’ve seen in the game. After the first couple of seasons and a Zombie looter-shooter game mode that missed their mark, the game found its groove.

Currently, Call of Duty: Mobile releases monthly-based seasons with varying themes and introduces new characters, new weapons, new Operator Skills, new Scorestreaks, new Perks, and new game modes. Starting with the third season’, the game developers named each season and battle pass in line with a central theme. The introduction of themes opened the cosmetics based monetization as the game wasn’t so restricted anymore by its modern military theme. After all, how many variations of camo skins for your M16 do you really want? It still took the team a few months and a few tries to get it right, but with Season 6 (and some lock-down tailwinds) monetization really took off.

Call of Duty Mobile let lose on their strict military setting with seasonal content. The results were fantastic.

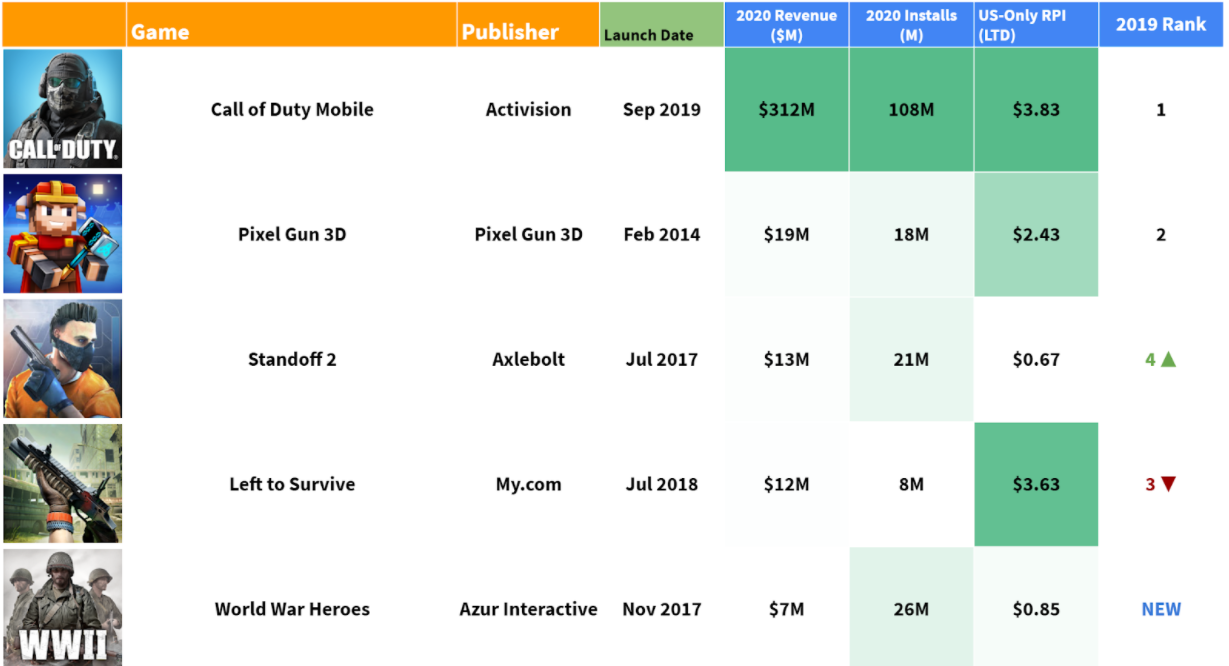

Call of Duty: Mobile takes around 75% of all the sub-genre revenues in the Western markets. To put the dominance in perspective, CoD generates 16 times more revenue than the #2 grossing FPS shooter title (Pixel Gun) in the Western markets. And while there are games that have found their niches with either strong PvE progression (Left to Survive) or focus on specific geography (Standoff 2 big in Russia) it is very hard to see a challenger for CoD in the near future. The most likely way CoD will ever be challenged in any way is through a substitute product, perhaps a different type of a shooter, rather than direct or indirect competition.

Tactical Shooters

Tactical shooters are considerably smaller than Battle Royale and FPS/TPS titles. Games in the sub-genre typically have the same 5vs5 game modes and loops as classic PvP, but add significantly more depth to their loadout system. Yet what really makes tactical shooters different is the speed (or lack of it) of gameplay and power progression. In a way, they can be categorized as shooters for older men whose reflexes are slower and whose wallets are fatter.

All of the successful tactical shooters operate a gigantic vehicle (tank, robot, ship), which naturally leads to a slower speed of movement and aiming. This makes the game more accessible for mature male players who like to take their time to make their shots. Slower core gameplay also increases the tactical aspects and creates more demand for team play. Both elements are highly appreciated by the target audience.

There’s always a very steep class-based power progression curve where a better tier vehicle has more armor, more health, and more firepower than a lower-tier one. This is again done with the target audience in mind who appreciate skill elements but tend to appreciate winning even more. Power progression also unlocks tremendous retention and monetization potential compared to Battle Pass, which doesn’t help a less skillful player to win.

While technically players can buy better tanks and robots, this genre keeps things competitive by having a clear rock/paper/scissor balance between each class. So while there is a clear power progression component where you can pay to have a better vehicle, there is also a high skill ceiling in the core gameplay where any team can win if they leverage the strengths and the weaknesses of each playable class.

The power progression, more mature audience, and deep chase for playable classes all lead to this genre having at least twice as large revenue per Install than Battle Royale and FPS/TPS titles.

We expect this genre to continue largely the same in 2021. The top titles are all very mature and given the limited size of the market, the low RPI, and the extreme amount of PvP content needed to compete against the existing top titles, it’s not a genre worth entering for anyone.

Snipers

The last and smallest sub-category for shooters is Snipers. While it's been around the longest on mobile and has the most mobile-friendly design, there really hasn’t been all that much innovation here. Our assumption is that the majority of players have moved to the other categories (PvP Multiplayer) and would rather play there. Mobile tastes have changed.

The biggest advantage for these games is that they are very “content-driven” - plus their content has a large audience and is very straightforward. Users walking into a sniper game are clear on what they want: aim-zoom-shoot. And monetization on these titles mainly depends on successfully leveraging this demand for weapons and upgrades. Snipers is one sub-genre that requires the least amount of control complexity, and, because of that, typically has the biggest opportunity to integrate systems that add progression depth and improve replayability.

The Sniper market has stabilized in the past year with Downloads and Revenue trends pretty much flatlining. Year-on-year, 2020 Revenue was slightly up (+8% YoY). This seems to reflect the lack of compelling newcomers rather than a market saturation.

The fact that a handful of games account for such a large portion of the sub-genre suggests there is an opportunity here to occupy this “casualist” demand for shooting games with low complexity. This is further reinforced by the fact that the current leader in the sub-genre is starting to get dated. Sniper 3D was released in 2014 and remains the sub-genre leader despite having low production value and dated F2P designs. It still relies on a very linear progression system - like the original CSR or Deer Hunter - and the content produced lacks flexibility. For example, the game doesn’t do a great job at reusing levels and fostering replayability. All that suggests there is an opportunity in the sniper sub-genre for new ways to create systems to acquire content and new gameplay designs to further leverage replayability.

The strength of this sub-genre rests on its mass appeal and simplicity. Gameplay in sniper games is very straightforward - and that’s probably what the audience is looking for. The value of the content driving monetization is also very clear and direct. Players will spend for a better weapon, and a better weapon will do more damage, shoot faster and zoom further.

The challenge is therefore not to find a way to make the content more valuable or appealing. The opportunity lies in the level of systems that facilitate the monetization of those weapons. That’s why historically direct purchase has been a staple of that sub-genre. Gacha - and the complexity and uncertainty that comes with it - might not be a natural alternative to that acquisition model. However, in the last few years, there have been some key innovations in the ways to monetize via engagement and in-game action. Battle Pass is the main one that comes to mind, but as “Sniper Strike” demonstrated there are other ways to bring higher-performing monetization models to these types of games.

The casual-ish, “mobile-friendly” nature of Snipers is reflected in lower RPIs/LTV. But there is a business opportunity here nonetheless. The strong appeal and large TAM of this sub-genre is also reflected in comparatively lower CPIs. The fact that the genre leader is relatively old with low production value - and that there have been few significant new entries in the last few years - suggests that this sub-genre is ripe for new entries and disruption.

For a while, Deer Hunter seems like the best contender to take that spot (despite the fact that the title has already been in soft launch for over a year). In its last quarterly report, Glu expressed its belief the title could be making a meaningful impact in terms of revenue for the first year, with the potential to grow to over $75M in net bookings in its second year of operation. But there’s already Hunting Clash from Ten Square Games and if this game becomes as successful as Fishing Clash from the same publisher, Glu’s Deer Hunter will have a very challenging time.

*in our taxonomy we track hunting games under sports, but it makes sense to mention them under sniper games as well due to identical gameplay

Reviewing Our Last Years Predictions

#1 Apex Legends on Mobile will not break into the Top 3 within the Battle Royale Category

Correct. But not relevant.

They haven’t launched the game yet. We’ll check back when they launch. Our Prediction stands when they launch the game, especially now that Warzone has overtaken them on PC and Console.

#2 Fortnite will no longer be the #1 across mobile, PC, and console by the end of 2020

Correct. But we got the specifics wrong.

Fortnite is no longer the top-grossing game. According to Superdata, the top games of 2020 were (1) Honor of Kings, (2) PUBG Mobile/Peacekeeper Elite (3) Roblox.

Although we got the specifics wrong. We expected there to be continuing declines for Fortnite through 2020, but that was incorrect. They grew through 2020, especially considering they were one of the main beneficiaries of stay-at-home lockdowns. They continued to deliver on amazing in-game events, and industry-leading cosmetics now with IP tie-ins. The main drop-in (publically visible) revenue was due to leaving iOS in Epic’s battle against Apple. Regardless, Fortnite had an amazing 2020, but other games had it even better.

#3 COD will make less than $230M in its launch year without better Cosmetics and launching in China

Wrong.

Sensor Tower estimates COD Mobile made $336M net revenue in its first year ($480M Gross). COD Mobile executed on cosmetics and didn’t need China to reach this astounding revenue milestone.

We expected that the RPI of COD Mobile wouldn’t break $1.00 within its first 12 months, and it wouldn’t break 230M downloads. They got 260M downloads and their RPI was $1.25, and they didn’t launch in China until the end of 2020.

COD Mobile dramatically improved their cosmetics pipeline, focused on themed cosmetics each season, doubled down on the tailwinds of COVID, and implemented their “Lucky Draw” system which dramatically improved the RPI. This translated into RPI growth faster than PUBG before they released in China. Now that they’ve released in China, we expect RPI to grow even faster.

COD Mobile dramatically improved their cosmetics pipeline and focused on themed cosmetics each season.

So huge kudos to TiMi and Activision -- they clearly executed on COD Mobile and continue to grow the game.

#4 The Top 5 Shooters in 2020 Mobile will be the same as 2019

Wrong. I should’ve clarified!

Mainly because I didn’t think this through. Obviously, by this point, we knew COD Mobile would be a hit in 2020. I should be comparing Q4 2019 to Q4 2020, not 2019 as a whole since then we wouldn’t include COD Mobile.

Also, we didn’t predict that Fortnite would get pulled from the store. So even if we’d included CODM, then Fortnite’s decline would have killed this prediction.

But our overall sentiment that this is a locked-up genre hasn’t swayed all. We’re waiting for that Lilith shooter to launch!

#5 Brawl Stars will continue to decline in revenue, but still, be the #1 Casual Shooter

Wrong.

Brawl Stars grew 28% in 2020, especially due to their launch in China (without which the growth would be around 4%). Unfortunately, the growth in China was temporary, as it seems they’ve gone back to their baseline of $30M/month in revenue. They continue to be the top casual shooter in the market.

#6 Tactical Shooter and Snipers will remain the smallest shooter markets with little growth in revenue

Correct. But they did grow substantially in revenue.

Snipers and Tactical made ~$300M in total, whereas BR and FPS made ~$3.2B. Big difference. Snipers only grew by 6% (even during COVID) where Tactical games grew by 31% likely due to COVID,

#7 Snipers will see a small download and revenue bump from the “Deer Hunter 2020” launch, but the rest of the market conditions will remain the same.

Correct.

Although Deer Hunter didn’t release.

2021 Predictions

#1 Free Fire will be a Top 3 Shooter for 2021

*App Store and Google Play revenue only (excluding China, Japan, and Korea)

Let’s start with a controversial one. Garena Free Fire dismissed as “PUBG for lower-tier countries” has slowly been growing to the point that it’s contending for the crown of shooters.

Free Fire grew its monthly US revenue run rate 4X from Apr-20 to Dec-20 and was the top shooter in Dec in the United States.

However, when we look at worldwide stats, Garena Free Fire has a very low LTD RPI compared to other Shooter comps. Due to the RPI, one might conclude that Free Fire’s monetization is soft, content cadence is slow, or the feature set is lacking. But WW RPI is a misleading metric to judge a game on, especially when Garena grows differently than other games in the category.

Free Fire’s monetization and content cadence are in fact very aggressive and its feature set is at least on par if not better than its peers. Free Fire’s low WW RPI is a function of geographic reach rather than feature set or content cadence/quality. The game is very popular in lower monetization territories like SEA and LATAM and that drags its global RPI down.

If we isolate one country (USA) to normalize RPI, the story is very different:

Because 1) it can stack DAU with presumably one of the best long term retention curves in the industry, 2) delivers world-class merchandising and content cadence, 3) it discreetly and effectively sells power (unlike its peers), and 4) it found a way to break out of developing countries into higher monetization territories, Free Fire will continue to grow revenue aggressively and become a top 3 shooter for 2021.

#2 More Multiplayer Shooter games will introduce new progression verticals to drive RPI Growth

Metro Royale and a shift towards loadout depth and actual out-of-game progression in Multiplayer Shooters will be growing. I expect games to introduce more of these modes and even start filtering with selling helpful items for this progression. These may still be limited to seasonal limited time modes, but progression is coming to PvP shooters.

#3 Apex Legends, when it launches on mobile, will not crack the Top 4 in Shooters

We have nothing against EA or Respawn. They are an amazing team. Apex Legends is a great game. But even Vince Zampella can’t change the reality that the Multiplayer Shooter/Battle Royale space on mobile is already very mature and a red ocean, even for larger developers.

Apex Legends has continued to do well on PC/Console, watching their Twitch viewership is showing signs that they can sustainably stack their DAU season over season. However, their mobile port will now be competing against CoDM, Free Fire, Knives Out, Fortnite, and PUBG Mobile. RPI Growth in this genre tends to start low and then grow over time -- so even if they manage to carve out a niche of players and start growing as they do on PC, 2021 will not be the year they reach the Top 4.

* Please note writers familiar with the project have not contributed to this prediction.

#4 COD Mobile will reach over $900M in Net Revenue Lifetime by the end of 2021

CoDM made more than $350M Net within its first year and after launching in China on December 25th, is now on pace to reach $500M Net Revenue by February

So how much will it make in 2021? Looking at PUBG Mobile’s China launch as a comp, we can expect an acceleration of their RPI curve through 2021. We should expect them to break through $900M, and potentially even reach $1B if things accelerate in China.

#5 Tactical Shooter and Snipers will remain the smallest shooter markets

Not really a surprise -- but these categories can’t compete against Battle Royale and Multiplayer Shooters.

#6 New entrants with a focus on progression will find blue spots in the red ocean

Persistent demand that can be seen in the growing amount of installs outside the top titles creat opportunities for market entry. The key is finding ways to retain and monetize this audience without succumbing to competing head-to-head against the top players in the category.